The Massachusetts Gold Rush – Part 1

After watching with increasing wonder on Thursday and Friday last week at the ever-increasing bid valuations, we now know the winners:

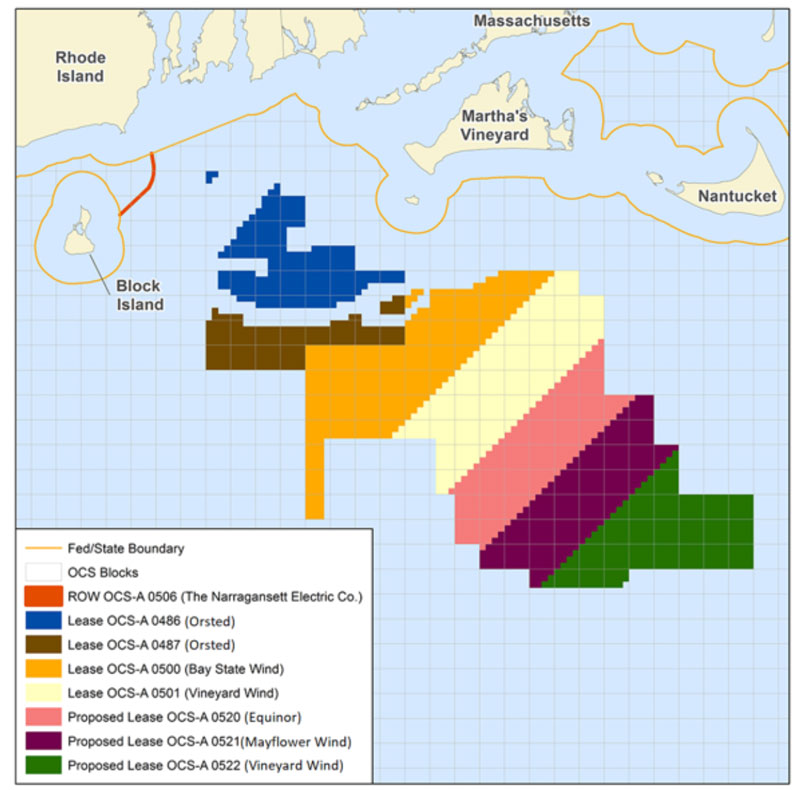

| Winning Bidder(s) | Lease Area | Winning Bid (US$m) |

| Equinor Wind US | OCS-A-0520 (128,811 acres) | 135 |

| Mayflower Wind Energy (Shell & EDPR JV) | OCS-A-0521 (127,388 acres) | 135 |

| Vineyard Wind (Avangrid & CIP JV) | OCS-A-0522 (132,370 acres) | 135.1 |

These record prices, a total of $405m, reveal how bullish developers are for the US offshore wind market. With 19 pre-qualified bidders and a large gap between this leasing round and another opportunity to gain leases, the appetite was proven to be voracious.

But what does this mean for the US market and are there any takeaways for other markets? In particular, the upcoming UK England and Wales Round 4?

The laws of supply and demand are like gravity – you cannot escape them

Equinor with their $42.5m bid for Empire Wind in 2016 shows that there is an appetite to pay high numbers for leases. But what we are seeing here is the result of the confidence in the US emerging market – and offshore wind generally – but with limited opportunities to develop projects. The level of competition and the final prices considering the long-term delivery of the projects are also good indicators on how bullish developers are on future technology costs, energy policies, commodity markets and power prices.

Furthermore, with Ørsted’s acquisition of Deepwater Wind earlier this year, the competitive picture in the nascent US Offshore Wind sector narrowed significantly towards large Europeans with global pipelines.

This allows the importance of scale, which is one of the important cost reduction factors in Europe, but also makes it difficult for smaller players to emerge. In the US this could mean fewer domestic developers.

Therefore, the market will welcome EDPR and Shell’s entrance on this Massachusetts leasing round. Also, the intense competition and deep pockets needed make this alliance look like a sensible decision. Indeed, the combination of EDPR’s renewable energy project development experience, with a pipeline of more than 5 GW in the US, and Shell’s experience in the US oil and gas sector represents a good strategic and operational move.

Too few leasing rounds planned

Looking ahead, we believe there are too few leasing rounds being planned in the US to build an industry with sufficient scale to provide the domestic supply chain the opportunity to develop to the scale it could, but also to give smaller and domestic developers an opportunity to get footholds in this market.

We would like to see 2,000-3,000 MW per year being offered for leasing, but at the moment the tap is being held to a much reduced flow.

This drives the bid valuations we have seen this week and the supply and demand element is clearly there, as we noted before. The lack of planned leases is combined with increasing offshore wind energy targets in Northeastern States with Massachusetts aiming for 1.6 GW by 2027, New York 2.4 GW by 2030, New Jersey 3.5 GW by 2030 and Virginia 2 GW by 2028.

This demand is materialised with the abundance of offshore wind energy tenders to buy that electricity currently being held or just about to commence. In this sense, New Jersey is taking the lead with a tender of 1.1 GW closing at the end of December 2018 and New York with one of 800 MW opening in February 2019. Other states are also awaiting the winners of recently closed tenders for renewable energy projects in general, as it is the case of Rhode Island, and for zero carbon energy in Connecticut, with the participation of offshore wind projects in both cases.

This is not a surprise as the cost of power in the North East, especially New England, is among the highest in the continental US. Thus, there is a clear road to market for offshore wind energy projects there. This momentum completely differs from 2015 when those sites were leased together with Vineyard and Bay State Wind but did not receive any bids at that time.

On one hand it looks fantastic for offshore wind (and the US Treasury) and the hunger for leases in this new market is evident. But it does not reduce LCOE with such a high cost simply for the right to develop a zone. This, compounded with limited leases being offered to the market, means less opportunity for a domestic supply chain; less opportunity for Jones Act compliant vessels etc. Again, this is not helpful in reducing LCOE.

This now sets the scene for the next auction in the US, probably being in the New York Bight in 2020. Will Massachusetts have sated demand at this level, or is it a benchmark to be equalled or beaten?

Finally, what does this mean for other leasing processes in more mature markets that combine pre-qualification with bid valuations and flexibility in the selection of the areas but overall cap on capacity, such as the UK’s Round 4? This will be the main topic of our next blog article ‘The Massachusetts Gold Rush – Part 2’ (published early January 2019).